Despite the unprecedented changes in our economy and workplaces in the past year, innovation is actually down in most industries.

This is problematic for the economy as a whole, but it’s especially bad for the many businesses who have fallen prey to the innovation freeze. That’s because many of these companies have been operating under the false premise that no one else is innovating either.

The truth is the playing field is not level, and those companies who were able to adapt didn’t wait—they accelerated in the face of uncertainty. Those who froze, stopped, or paused—hoping to ride out the pandemic until they could get back to business as usual—are in for an unpleasant reckoning… and not just from Amazon’s $400B surge or Microsoft’s $270B increase (in just the first half of 2020!)

The gains made by these and other tech giants are no surprise. But other players that stalled companies need to be worrying about aren’t even on their radar—and it will come as a shock when they discover who is eating up their market share.

But before I explain that, how do we know innovation is down? Anecdotally, I can see it in the conversations between executives in my coaching communities and masterminds. Some are finding a creative path forward, but most are stuck, having slashed all funding for growth and innovation since last March.

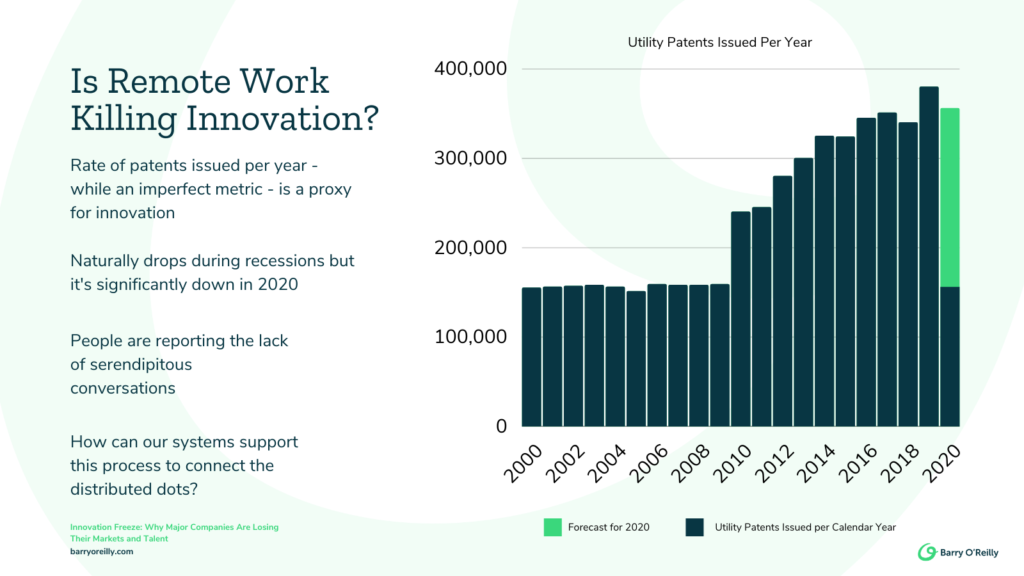

On the quantifiable macro level, we can see that patent registrations have dropped precipitously, to levels not seen since the early 2000’s. Patents are leading indicators that investments in research and development will bare fruit, creating new products and future growth. The rate of patents issued is not a perfect metric for innovation, but it’s a well-known and useful proxy that economists observe.

When I show this chart to executives, they’re shocked to see how big of a drop there really was in 2020. But what should be even more alarming is what we can expect in the next few columns.

Typically after recessions—such as in 2000, 2007, and 2011—it takes two or three years for the rate of patents to recover. With such a significant cutback now, economists and executives are worried about the future like never before.

Three Archetypes of Innovation

So while legacy companies are lagging, who’s leading and innovating their way out of the crisis and into strong growth? From my perspective, businesses are falling into three basic categories in regards to innovation: Leaders, Stallers, and Reinventors.

Leaders

At the top, unsurprisingly, technology companies make up six of the ten businesses that have seen the most growth during the pandemic. These Leaders are remote-ready and well-structured for rapid, data-driven innovation in a fully digital economy. A remote-enabled work environment is table stakes for SalesForce, Zoom, Paypal, Slack, and their ilk (The Home Depot is a notable outlier in the top 25). The success of these companies has only accelerated.

Stallers

Next we have a wide range of enterprise-level companies who have struggled for years with ineffective digital transformations: transportation, financial services, traditional retailers, and many others. Most of these businesses pulled funding for growth and innovation the moment the unanticipated hit.

They underestimated the time it would take for the pandemic to run its course and assumed consumer behaviors would quickly return to past patterns. They’ve also struggled simply to keep their operations afloat, let alone foster innovation in this remote-work reality everyone around the globe is becoming conditioned to—and will likely continue to expect (or demand).

These companies are losing ground to the tech-enabled giants as well as rapidly scaling businesses like cyber-security firm CrowdStrike, which is pivoting its business model (providing cyberattack response services to enterprises) to grab more adjacent market share by offering increased remote-machine security for work-at-home situations.

Reinventors

But the real surprise is that the Stallers are also beginning to face competition from the third category of companies: those who previously had minimal involvement with the digital economy but are starting to reinvent themselves to become something even better.

These late-comers are leapfrogging legacy technology and empowering their teams for innovation—pivoting and even expanding their value propositions!

For example, a European auto parts company previously had a large backlog of service contracts. Its small team of highly specialized technicians who would travel wherever needed to personally repair complex machinery. Since COVID, this company started utilizing virtual reality to allow its senior techs to guide less-skilled on-site mechanics, enabling them to scale dramatically and offer this kind of training as a service.

So here’s a company that used to just sell auto parts but has now embraced new technological capabilities to develop an entirely new class of revenue stream. This is happening in every sector, and these forward-thinking companies are starting to add to the disruption of their industries.

Why is Innovation Down in Large Organizations?

Time is short for Staller companies that have been frozen in place since the first lockdowns. To shift back into “drive,” you have to recognize a few patterns that are likely keeping you stuck.

- Funding Slashed

If you cut funding for growth initiatives in order to wait and see what happens, you’re shooting yourself in the foot. You have literally stopped yourself from being able to move forward and find your way through the new economic landscape. You cannot wait any longer—you need to act and learn your way through the uncertainty to determine what your future will look like in the world ahead.

- Lacking tools for remote collaboration

If you were previously reliant on in-person communication at the office, you’ve got to invest in the best tools to help people work together anytime from anywhere. I’ve encountered teams where simply getting their home laptops to connect to the company system or have four people on a video call were a major undertaking.

Every minute spent trying to figure how to collaborate is a minute people aren’t working on the problems to move your business forward. Those minutes quickly add up to months of effort and mountains of lost money.

And remember, your talent compares their social collaboration tools to their business collaboration ones. The wider the gap, the greater the frustrations, and the sooner they look elsewhere to work.

- Lacking the capability and processes for remote collaboration

Managers are too used to monitoring people’s activity in-person, measuring success as tasks completed and managing outputs rather than outcomes.

The command-and-control model has been outdated for decades, and in a remote environment it’s impossible to replicate. So instead, managers constantly ask team members for updates. This is wasted effort—squashing creativity, damaging morale, and stopping your company from profiting from remote productivity.

7 Ways Stalled Companies Can Get Back on the Road

To overcome these patterns, you need to start now. Don’t wait for COVID to end, because every day that goes by, you’re losing ground to those who are forging ahead.

1. Start designing and testing how people can work differently.

This will be a differentiator. Even if your employees come back to the office at some point, many workers are in favor of 3-2-2: work for three days in the office, two days remote, and two days off.

You’ll lose talent without work-location flexibility. Companies like Pilot.co are helping companies hire people from anywhere and deal with the legal and logistics of remote-work employees.

2. Start over-communicating across your business what is happening, how you’re responding, and the direction you want people to go.

When the pandemic struck there was no better example of crisp, scalable communication than Arne Sorenson, President and CEO of Marriott International.

3. Your ability to move information and keep people aligned and engaged has never mattered more.

For example, the founders of Slack and Atlassian frequently send out short video updates, to support longer form updates and all-hands. Small, frequent informational updates help people choose when it matters most to them to dig deeper.

4. Invest in the best collaboration tools for your teams’ use.

The more visibility you can provide them about what others are doing and why, the better. Great tools let people focus on their work rather than continuous updates to managers about the tasks they could, should, and will be doing. Get people working, not spending time figuring out how they can collaborate together.

5. Design collaboration into your operations.

Get intentional about how you’re organizing collaboration. Enable and encourage cross-functional conversations and include “wildcard” people in meetings to get different perspectives, challenge assumptions, and raise awareness about new solutions. You’ve got to provide opportunities for people to connect dots and experience synchronicity in a remote environment.

6. When onboarding new hires, work hard to build their network in the company.

Give them a buddy. Help create the connections they need to be successful by pairing them with people who’ve been in the company for a longer time and have strong connections to others.

7. Make as much information as you can as transparent as possible.

Innovation happens when people join disparate dots. Make sure leadership is clarifying and communicating desired outcomes and individuals are sharing what actions they’re attempting to achieve them.

I know that this has been a difficult time for many company leaders, and making the kinds of changes necessary to compete in this new world can seem daunting. It requires a healthy dose of unlearning, but it is possible.

For inspiration, check out my podcast episodes in which I explored these topics with leaders from American Airlines and Wells Fargo.

American has achieved an array of measurable successes in the midst of the pandemic, such as rolling out hundreds of contactless kiosks in weeks and developing the capability to update them in real time.

Wells Fargo was able to pull together a small, cross-functional team to swiftly handle business loans for the Paycheck Protection Program which was dropped in banks’ laps by the US government last spring.

You’ll be inspired hearing how these companies have managed to shift out of ineffective legacy processes and built capabilities for rapid innovation.

You Can Do This

Hitting pause on innovation was never going to be a good bet, and if that’s your situation, it’s high time to get back in the game. Your competitors aren’t waiting.

Remember, think BIG, but start small so you can learn fast. If you need help to get the ball rolling, reach out and let’s chat.

Here’s to getting unstuck,

Barry